Regulation - A Delicate Dance

Regulation - A Delicate Dance

Why regulation is needed for the continued growth of the crypto industry

Disclaimer: Any views expressed in the below text are the personal views of the author/s and do not constitute investment advice or recommendations for investments. The author/s views should not form the basis for making investment decisions - invest in markets at your own personal risk after performing thorough due diligence.

The free market is the core of the global economy. It’s the nuclear reactor that has powered our journey from humble hunter-gatherer beginnings to the industrious force of nature we have become today. Some may debate whether this ascent is a good thing, but the uplift of billions from poverty and the marked improvements in average global quality of life cannot be denied. Nuclear reactors need regulation to prevent catastrophic failure and atomic annihilation. Markets are the same. Regulations act as the coolant, controls, and safety valves, ensuring this force of nature is being harnessed beneficially. Without these mechanisms, meltdown is assured and nothing more than an uninhabitable radioactive wasteland will remain. This wasteland can be perfectly visualized through most market participants’ portfolio performance in the digital asset space so far for 2022.

So, what is the purpose of regulation? This simple question is one of the most misunderstood in the crypto space. The average crypto enthusiast will tell you exactly what they think of regulation, regulators and the institutions responsible for enforcement. This pillar of global markets is often seen as a group of overzealous quasi-politicians and government officials squashing the dreams and aspirations of the young upstart at the behest of some shadowy institution or cabal. Though this may be true in some cases, it also represents a fundamental misunderstanding of the role of the regulators.

Regulation and regulators do not exist to regulate technology. They exist to regulate the possible human behaviours when using said technology. When viewed through this lens, the purpose and necessity of regulation are readily apparent.

A comprehensive understanding of the global regulatory environment should arguably be at the core of any research that one is conducting when making investment decisions; without that understanding, it is impossible to forecast where value may lie accurately. This point is relevant in all markets, not just in digital assets. To that end, the purpose of this article will be to provide you with a comprehensive understanding to equip you with the necessary details to evaluate the global regulatory regime, highlighting differences and recent developments in some notable jurisdictions. We’ll then give some perspective on where we think things are headed and share some comments from some of our partners. Equipped with this information, you’ll be in a far better position to understand the ever-evolving game of chess between regulator and market participant. Let’s dive in.

A Side Serving of Economics

In light of recent market, geopolitical, monetary and social events, the economy is in the limelight, but what is “the economy?”

Figure 1 - Supply, demand and price dynamics visualised. Source: Investopedia

At its most grossly oversimplified, the economy can be thought of as the system by which goods and services (resources) are bought and sold in a given region. The ratio of these resources varies greatly worldwide. The dynamics of supply from businesses/producers and consumer demand come together in a beautiful symbiotic dance to form what we know as the ‘market’.

The market is the mechanism by which prices are established for goods and services, resources are distributed and trade is facilitated. In a perfect world, this complex mechanism would function in an efficient and fair manner for all, ensuring that the right value is assigned to the right goods at the right time as dictated by the dynamic interplay between supply and demand. However, we do not live in a perfect world and markets of this nature do not form organically for one simple reason - people.

Supply and demand are second-order effects that are dictated by human behaviour. This human element gives a market its dynamism and drives volatility. It is also this element that necessitates regulation. Without regulation, global markets would be significantly more inefficient, unfair, risky, unstable and full of unscrupulous participants. Many of these attributes can be said of the current state of digital asset markets. Through regulation, markets become fairer, higher standards of service and product can be achieved and maintained, risk and fraud can be reduced and overall efficiency can be improved.

Figure 2 - Source: New York Times, Faith In An Unregulated Market? Don’t Fall For It.

At this point, we must acknowledge those who may disagree with everything that has just been written. Many arguments can be made for reducing or even removing regulation from some markets and some of those arguments have merit. Not all regulation improves market efficiency or fairness and can sometimes even have the opposite effect. We postulate that this is because regulation is ultimately designed and implemented by humans - we are nothing if not fallible. The definition of efficiency is also subjective to a degree, but we digress.

The meteoric rise in the importance of technology and connectivity in our daily lives in recent years has driven global changes few could have foreseen, leaving the economy unrecognisable. Few sectors have avoided the disruption technology has wrought; this presents a unique challenge for politicians and regulators. Though political views and perspectives vary, the common goals of economic growth and improved quality of life are universal. To achieve these goals concurrently, policymakers have the unenviable task of presiding over an extremely complex global economic system.

Globalisation has brought nations closer together than ever before and the speed with which changes in different areas of the economy can be rendered by technology is profound. The legendary hedge fund manager Ray Dalio explained the various factors at play in a recent video below. Of all the economic subdomains highlighted in the video, innovation is arguably one of the most important. This is where things get dicey for politicians, given the speed and ferocity with which technology drives change.

Innovation Whiplash

At its core, innovation is looking for new ways to solve old problems or reimagining old systems with new technologies. This can be problematic as these old systems tend to form integral parts of the economy, and the changes that will be delivered may not be politically or socially desirable. The second challenge policymakers face is that innovation is inevitable. If regulation is too harsh, restrictive or heavy-handed, the economic benefits of an innovation may be lost to a different region or nation, competitor or otherwise. Managing the delicate balance between capturing economic benefit and maintaining the status quo is the key problem that regulators and policymakers face.

Figure 3 - Source: https://www.migso-pcubed.com/blog/pmo-project-delivery/four-step-risk-management-process/

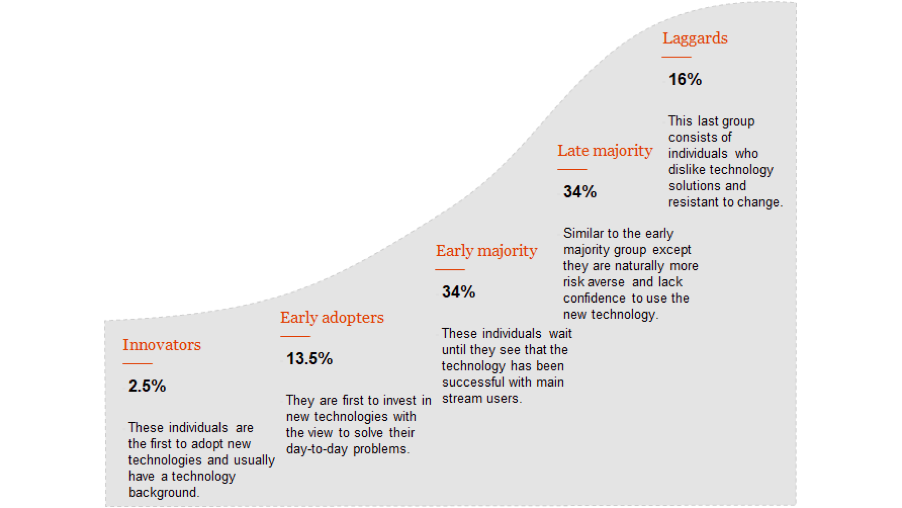

A significant part of this task is risk management. In the context of innovation and new technology, this is where the true challenge for regulators lies. As detailed above, a core aspect of the risk management process is identifying and assessing potential risks. The problem with new technologies is the limited context in which this identification and assessment can take place. When this is the case, politicians and regulators are left in a reactive position, and decisions can seem heavy-handed or misinformed. New technology also tends to be inherently difficult to understand, which, coupled with early adopters' nature, makes regulation even more challenging.

Figure 4 - Source: https://www.pwc.co.uk/services/economics/insights/vr-ar-to-boost-global-gdp.html

Innovators who blaze a trail with new technologies are generally subject matter experts. This also tends to mean that whilst they are brilliant technologists, they can be terrible educators. The reasons for this are many but can be boiled down to the relative complexity of the mental models these individuals leverage to use the new technology and drive innovation forward. A deep understanding of the many facets of new technology and the interplay between these factors is generally not something that is easily explained or understood, yet it is intuitive to them. This is because the total amount of knowledge required for in-depth understanding is vast, and the mental relationships between these discrete areas of understanding are equally complex.

What is evident to the expert is impregnable to the beginner. As such, the level at which an expert operates is unattainable for a beginner, as the expert will simply be unaware of what a beginner needs to know. They operate at too high a level to comprehend what a beginner could struggle with.

As an addendum, this is also why education lies at the heart of many crypto marketing strategies. Marketing uses analogies to help people understand new products and their benefits, but if there are no parallels that can be drawn, then materials need to be kept really basic.

In the context of regulation, the first-mover tends to wield a large amount of power when shaping regulation. This is due to the amount of value captured and the subsequent influence that tends to come with that value capture. An excellent example of this outside of blockchain is the influence of social media, socially, politically, and otherwise. Any time there is a hint of regulations being implemented that may be disadvantageous to the companies being targeted - out come the lobbyists. This, again, puts the regulators in a reactive position, and reactivity creates unease which is problematic as regulators do not like to feel uneasy. Couple this with being confronted by an individual who has made a technology capable of moving billions of dollars worth of funds outside of existing systems and structures yet cannot explain how it works, what it’s for, or why it’s needed. Then throw in some geopolitical headwinds, a black swan event or two, and you have a ticking time bomb, ready to ignite, yet made of unknown explosives with unknown effects and an unknown impact radius.

Regulating the Magic Internet Money

This brings us nicely to probably the most pressing question that needs to be answered both by and for regulators: what is crypto? For those of you reading this who are actively involved in the digital asset space, the answer to this question may seem obvious, yet if you are a regulator, things are not so clear-cut. How crypto is defined varies significantly across jurisdictions and even within jurisdictions. In this section, we will be exploring just how much inconsistency there is in the regulatory space at the moment and why this is detrimental to the overall development and adoption of the technology.

The US

Figure 5 - Gary Gensler, Chair of the SEC. Source: The Financial Times

Taking the US as an example, there is no single consistent definition of what crypto actually is. Different government agencies have different categorisations for the new asset class. The SEC argues that many crypto assets are securities, the CFTC views Bitcoin as a commodity, the Treasury thinks it’s a currency, and the IRS is vague in their definition but definitive in its desire for tax revenue from whatever it is.

Recent developments, however, indicate that this sea of contradiction may finally be parting. A wide-reaching, bipartisan crypto bill finally emerged on the morning of the 7th of June from Sen. Lummis and Sen. Gillibrand. This marked a significant stride forward for progressive/accommodative regulation and is a major improvement on the restrictive policy currently in place for many developers and stakeholders in the space.

Below are some of the key points from the bill from our perspective:

· The bill requires a deep study into the power consumption of digital assets, helping to determine the most effective ways that bitcoin can help society move closer to achieving climate goals, reducing energy waste and utilising more renewable sources.

· The bill encourages the usage of bitcoin and digital currencies as a medium of exchange. It provides a tax exemption for transactions of up to $200. Bitcoin adoption in the USA will increase if BTC can be used to buy groceries, gas, and other necessities without having to pay capital gains taxes. This number should be higher and will likely rise in the future, but any exemption is a step in the right direction.

· The bill defines a framework for differentiating which digital assets are commodities and which are securities. It uses the Howey Test to determine that a given asset is *not* inherently a security. As such, if the SEC wants to claim that a given digital asset is a security and not a commodity, it needs to go to court.

· The majority of large digital assets will be classified as commodities and fall under the purview of the CFTC, whereas the SEC will oversee the securities. The CFTC will have exclusive spot market jurisdiction over all digital assets classified as commodities, whilst exchanges will register with the CFTC to conduct trading activities, abiding by the relevant rules and frameworks. BTC and ETH are commodities under this bill. A US spot ETF is likely in 2022 if this bill is approved.

· On the spot ETF point - Grayscale has just retained Donald B. Verrilli, Jr., former Solicitor General of the United States, as additional legal counsel alongside Dasis Polk in the conversion of $GBTC to an ETF. This combination will put huge pressure on the SEC to green-light the first spot bitcoin ETF in the US.

· SEC and CFTC are tasked with studying and reporting on creating a self-regulatory organisation (SRO) that could complement the regulatory work. They are also tasked with developing cybersecurity guidelines for digital asset service providers.

· The bill states that miners are not to be seen as brokers, and bitcoin obtained from their activities is not to be treated as income until converted into fiat after their “disposition”. It also specifies that digital asset lending agreements are not taxable events. This is perhaps one of the critical points of this bill. A gold mining company isn’t taxed until it sells its mined gold. Current legislation taxes bitcoin as income the moment it is mined. This is both nonsensical and unfair. It forces the bitcoin miner to sell extra bitcoin into the open market to pay said tax. This might cause a second taxable event, a fan favourite, capital gains for the duration of holding the asset. It is bad for the profitability and long-term health of bitcoin mining operations in the United States. It is also bad for price action and long-term holders as bitcoin miners are forced spot sellers. Removing income tax on bitcoin mining rewards would result in more miners holding their bitcoin for longer and a feedback loop leading to a greater positive price impact.

· Self-Custody - the bill grants the rights to an individual to keep and control the digital assets they own. In our view, gold has failed over the last decade as an inflationary hedge (we will touch on this in further articles) partly due to us storing it all in banks either by government decree or so we could have access to paper money. Executive Order 6102 is an executive order signed on April 5, 1933, by US President Franklin D. Roosevelt "forbidding the Hoarding of gold coin, gold bullion, and gold certificates within the continental United States." This was only repealed in 1974. As Bitcoin doesn’t need banks as custodians, it would be unnecessary, ultimately leading to Bitcoin failing the same way as gold in 1933. The ability to self-custody is the most important part of this bill. We need to self-custody to protect the long-term health of the Bitcoin Network.

· The most recently added provision is topical and is something we wrote about in 'The Lehman Moment'. Stablecoins should require issuers to hold US dollars or dollar equivalents to enable redemption by the customer at any given time.

The above shows that the US is gradually taking steps to understand and direct the blistering evolutionary trajectory of the digital asset space. However, the above bill is simply a proposal at this stage, and many find it both concerning and farcical that over a decade into the maturity of a new asset class, policymakers in the US still cannot agree on what crypto actually is.

Read the full bill here.

Europe

Figure 6 - Ursula Von der Leyen, President of the European Commission. Source: The Financial Times

The European Union is nearing an agreement on key legislation to regulate the cryptocurrency sector that would set common rules across the 27 member states. Markets in Crypto-Assets - (MiCA), first presented in 2020, will put European regulators at the forefront of supervising cryptocurrencies by creating unified rules across the $17 trillion continental economy. Addressing issues such as investor protection and crypto’s impact on financial stability has taken on added urgency after last month’s collapse of the UST and the issues this month with lending platform Celsius.

France and the European Parliament are optimistic about resolving the remaining issues in the MiCA package and reaching a deal this month. Negotiators are expected to meet on June 16 and June 30.

Member states and the parliament still disagree on several critical aspects of MiCA:

· The inclusion of NFTs within the framework

· Stablecoin regulation

· Supervision of the largest crypto-asset service providers, or CASPs

Both sides are also discussing how to limit the use of stablecoins as a payment method by introducing a ceiling, particularly for transactions not denominated in Euros. This could be an attempt to pave the way for the long anticipated European CBDC proposals. Though there is limited public information on what these proposals will look like and the impact they will be designed to have, we know the EU is pushing forward with research into the applications of CBDCs. As they are already in use in several countries worldwide, and EU policymakers will not wish to be left behind, it is safe to assume that a CBDC is on the horizon.

Our primary concern within MiCA is the following extract: “Issuers of asset-referenced tokens or crypto-asset service providers shall not provide for interest or any other benefit related to the length of time during which a holder of asset-referenced tokens holds asset-referenced assets." This confers that lending providers such as Celsius, Nexo, BlockFi etc., will no longer be able to provide interest on stablecoins. This clause could be in an attempt to prevent the seeding of business to the crypto industry from legacy banking providers due to the unattractive interest rates they offer.

We have noted that much of the regulation is being pitched as "consumer protection" rather than as a direct response to any threat crypto poses to the monetary/financial systems. It's also worth noting that the European Union member state's total population is 440 million. Whilst the USA's is around 330 million. Although the financial might, global reserve hegemony, and power of the USD are ever-present, due to the slow uptake in the categorisation of digital assets, we wager that the EU will eventually lead on this issue. Every entity within the EU will likely follow MiCA. Alongside this, because of the “Brussels Effect”, we feel there is a good chance these rules will eventually become international standards. While everyone is focused on the US and China, the EU is casually leading the way. If the EU leads, other countries will follow and eventually, the US will have to follow suit or risk being left behind.

Overall, we are pleasantly surprised with how EU lawmakers have so far dealt with cryptos. Highly knowledgeable civil servants have clearly written MiCA. It has been endorsed by EU Ministers of Finance with a more open approach to blockchain and cryptocurrencies than their non-EU counterparts. The EU made the mistake of allowing the US/Asia to dominate the tech industry. They do not want to repeat this mistake with the cryptocurrency space.

Read more about MiCA here.

Special Mention: Malta

Figure 7 - Source: Welcome Center Malta

It’s worth mentioning that whilst the overall European Union has been relatively slow in regulating activity in the digital asset space, some countries within the EU have been far more agile. Malta is one such country, and as a country with a long history of rapidly adopting and regulating new technologies and innovations, this openness to the potential disruption that blockchain brings makes sense. The embrace also happened far faster than anywhere else, with the laws establishing the regulatory framework being passed in 2018.

The bills were designed to position Malta as a European hub for blockchain, crypto, and other associated technologies. The Maltese Parliament passed the bills unanimously, and the prime minister at the time, Joseph Muscat, tweeted, “We aim to be the global trailblazers in the regulation of blockchain-based businesses and the jurisdiction of quality and choice for world-class fintech companies.”

Malta was aiming to establish itself as an early pioneer in cryptocurrency's economic innovation, bolstering the country’s economy with a niche market for cryptocurrency companies. This move was widely received as a positive by the crypto community at the time, and Binance announced that it was looking to open an office in the island nation.

The problem is none of the goals were achieved in any meaningful way. The plan to transform Malta into the blockchain island in the Mediterranean faltered before it even began, even though the regulations were seen as very crypto-friendly. Despite the fanfare of being the place to incorporate to conduct Europe-focused business and the positive feedback from the industry, it never happened.

So, what went wrong?

Though the regulations were friendly, the implementation was less so. This is because while any given law framework is friendly on paper, the regulators conduct the implementation of that framework. In the case of Malta, the regulators were markedly less open than the frameworks may have implied. Binance was denied its license in 2020, and since the law's passing, only one company has received the necessary licensing and approval to operate legally in the country: Consensys.

This apparent contradiction was not well received by the crypto industry, and many industry participants have since turned away from Malta. Yet the risk-averse approach being taken makes sense when viewed from the perspective of the regulators and in the context of the 2018 crypto winter when the vote went through.

The Maltese regulations were the first of their kind, which put somewhat of a target on the back of the tiny island from other more powerful and influential nations with a far stronger viewpoint on how crypto should be regulated. It is not unreasonable to think that there may well have been some economic and relations consequences to moving so fast in rolling out the red carpet for an industry that was widely viewed as a glorified ponzi-scheme at the time. Though this viewpoint remains common, the business case and potential benefits are far clearer.

It was not all in vain, though, as if you compare the EU MiCA regulations outlined above with the Maltese frameworks, there are several undeniable parallels. Though Malta may not have captured the first movers advantage in taking this enthusiastic approach, the foundations for what is now being built and implemented may have been laid.

Read more about the Maltese regulations here.

UK

Figure 8 - Rishi Sunak, Chancellor of the Exchequer in the UK. Source: BBC

We feel that the UK’s stance on digital assets is currently one of the most progressive in the world. Recent comments from Rishi Sunak and Matt Hancock show a bipartisan willingness to create accommodative laws and regulations to foster digital asset innovation in the UK, thereby helping the UK retain its spot as one of the most progressive and frictionless places in the world to conduct business.

Although the UK confirmed in 2020 that crypto assets are property, it has no specific cryptocurrency laws, and cryptocurrencies are not considered legal tender. According to the Bank of England, since cryptocurrencies lack classical definitional characteristics, they are not considered ‘money’ and do not pose a systemic risk to the stability of the financial ecosystem. Over the years, the FCA, Bank of England and numerous tier 1 UK banks have issued a range of warnings and guidance about the use of cryptocurrency in the UK. Those warnings have primarily revolved around the absence of mature regulatory frameworks, the status of cryptocurrencies as stores of value, and the dangers of speculative trading, volatility and scams.

Although the UK has left the EU, cryptocurrency regulations will remain broadly consistent with the bloc in the short term. The UK will implement, for example, directives equivalent to the EU’s Markets in Crypto-assets (MiCA) and E-Money proposals, along with various AML directives. The UK previously transposed the cryptocurrency regulation requirements set out in 5AMLD and 6AMLD into domestic law. Accordingly, from January 10 2021, all UK crypto asset firms that provide services to UK resident clients have had to register with the Financial Conduct Authority (FCA). Critically, these groups must comply with AML/CFT reporting and customer protection obligations.

There has been friction with the attempt to regulate digital assets in the UK. On January 6 2021, the FCA banned cryptocurrency derivatives trading for retail customers to protect consumers from market volatility. In our view, this was a double-edged sword. On the one hand, the FCA achieved their overarching aim. On another, they prevented free market access to many bedroom traders who successfully navigated the Wild-West markets and learned invaluable skills.

In the future, the UK will likely diverge from EU cryptocurrency regulations. Statements made in the House of Commons in April of this year indicate this may happen sooner rather than later. London has long been the beating heart of the global financial system, yet Brexit has left retention of that crown uncertain. The exodus of many large firms to Frankfurt and other European cities has proven to be both a threat to London’s status and a golden opportunity to embrace new technologies. The gap left by banks moving their operations elsewhere means there is now plenty of space and appetite to become a world leader in blockchain technology. Comments and activity from the government and actions taken by the FCA, the Treasury, and the Bank of England, as well as a host of advocacy groups such as CryptoUK, demonstrate the UK is actively positioning itself as the place to conduct blockchain-related business on the European continent.

Read more about the UK regulatory announcements here.

Switzerland

Figure 9 - Source: The Financial Times

Switzerland is a core component of the global financial system, a fintech and blockchain hub, and has long been renowned as one of the most crypto-friendly jurisdictions. The Swiss approach to the regulation of DLT has been progressive, even amongst progressives.

On August 1 2021, the “Federal Act on the Adaptation of Federal Law to Developments in Distributed Electronic Register Technology” and the associated blanket ordinance came into force, making Switzerland one of the first countries in the world to enact legal regulations for blockchain. These regulations provide the legal certainty to drive innovation and growth, and with the rest of the world now playing catch-up, it is clear how forward-thinking the Swiss have been.

Read more about the Swiss laws here.

Liechtenstein

Figure 10 - Source: Freeman Law

Another crypto-friendly alpine country, or principality in this case, on the European continent, has also emerged as a welcoming jurisdiction for crypto business. Liechtenstein has arguably the most transparent regulation for cryptocurrency and related activities globally. PwC has also declared it as “having the most comprehensive tax policy on digital assets globally” for the second year in a row. Having such regulation makes sense as Liechtenstein has long been a business hub, with more companies registered than citizens. This is because though Liechtenstein is part of the EEA, it is not a part of the EU, and certain regulatory requirements are less obtuse as a result.

Liechtenstein began enacting a first-of-its-kind legal framework to regulate blockchain and associated technologies. The Token and Trusted Technology Service Provider Act (TVTG) provided a legal framework for new roles of parties and stakeholders in the industry and established common responsibilities. The law also describes the requirements for tokenisation services, the purpose and types of tokens, liability for non-compliance, and licensing, reporting, and registration requirements for tokenisation service providers. The law defines the tokenisation method and what a token actually is in the context of data flow in the Trusted Technology system, alongside the different types of rights or claims it represents.

The level of regulatory clarity Liechtenstein provides has us seeing a number of ambitious projects incorporating in the principality. These projects are looking to deliver value to underserved segments of the market. To identify these segments, one only has to consider the depth and breadth of services available in legacy markets, and then identify the gaps in the crypto space. Regulated and authorised financial professionals, for instance, cannot currently render their services in a compliant way. This means mid-ticket investors without the resources to outsource their investments to a hedge fund are being excluded, thus projects catering to this underserved demographic are building quietly in the background.

Read the full set of laws here.

The Caribbean

Figure 11 - Source: CryptoSlate

The Caribbean, namely the Cayman Islands, British Virgin Islands, the Bahamas, and Bermuda, are some of the most business friendly and tax efficient locales for a business to incorporate in. Alongside this - the physical proximity to the US makes incorporating digital asset funds and companies in this jurisdiction extremely attractive, especially so as the US (as stated above) is now slowly catching up with regulation and understanding of the asset class. This jurisdiction has long been crypto-friendly, and laws are continually refined to maintain competitiveness.

A significant portion of the economy on these islands is derived from financial services, so there is a vested interest to continue the value capture already being enjoyed. We expect to see continued agility in policy making and regulatory design in this region, as well as heightened compliance procedures being implemented.

Read more about the different regulations in the Caribbean here.

China

Figure 12 - Source: China Briefing

The examples we have presented so far have generally been progressive in approach. Despite the misgivings and fears of many politicians and regulators in the West, the regulatory environment has generally been favourable. Consumer protection is at the forefront of many regulators' minds, as well as systemic and localised risk reduction. This makes sense as politics in democratic countries is a popularity contest; it is not politically acceptable to lose out on the economic benefits of innovation through overly punitive regulation or to have your voter base repeatedly lose vast sums of money. When a democratic candidate or politician positions themselves as "pro-crypto", it’s not because they think it's some broadly popular policy position with any constituency. It is generally because they're looking to solicit a few large donations from one or two UHNW crypto natives.

However, when popularity is not a consideration, a different approach can be observed. China and India are two very different examples of a more rigid approach to regulation, and a demonstration of the impact regulatory decisions can have.

China has long been the subject of intense debate in crypto and blockchain circles, and rightly so, owing to how instrumental the Chinese market has been in historical cycles. That all changed in 2021 with another ban on trading digital assets. This was initially dismissed, as China has had a long history of banning and unbanning crypto. However, in May 2021, things were different.

As outlined previously, Bitcoin and crypto represent a way of transferring value outside existing systems. Conversely, blockchain allows for unparalleled granularity and accuracy in a user group's financial patterns and habits. In an authoritarian country like China, with strict capital controls and a penchant for surveillance, blockchain is both a blessing to be harnessed and a scourge to be eradicated. To that end, the rapid roll-out of the eCNY (数宁人民币) and the departure of some of the largest BTC mining companies from China in 2021 shines a light on the direction the CCP seem to be taking.

These decisions have not been without consequence. In previously controlling a large amount of the hashing power underpinning the Bitcoin network, the Chinese government wielded a large amount of control over the growing asset and, subsequently, the entire market. Though the mining companies were privately held, there is no such thing as a private company in China. Beyond a certain company size, CCP members must sit on the board and provide “ideological guidance” to “maintain harmony”. It is not beyond the realms of possibility that these individuals could have been used to manipulate the Bitcoin network. You might think the board could refuse. However, if they did, it is possible that the favourite catch-all law of “picking quarrels and provoking trouble” may have been broken, and then the fun could really begin. If you’re unsure what this fun might entail, look no further than Jack Ma and the cancelled Ant Financial IPO or the DiDi debacle from last year. With the exodus, this potential advantage is lost. The long-term impacts of this remain to be seen.

Figure 13 - The drop in Mainland Chinese hashing power following the ban. Source: Brave New Coin

Read more about Chinese regulations here.

India

Figure 14 - Source: Beyond The Posts

China isn’t the only country that’s pro-blockchain, anti-crypto. India has adopted a similar approach and perspective in recent years, as reflected by the apparent flip-flopping observed in the approach to regulation. Recent changes in tax laws and comments from various ministers in different branches of the government have been heavily criticised by stakeholders in the Indian crypto ecosystem. The criticism tends to revolve around an apparent lack of understanding from the policymakers and misinformation peddled by those in positions of influence. This problem is not unique to India, as a lack of education in regulatory bodies and politicians is a significant hurdle to overcome worldwide.

How things will evolve in India from a regulatory perspective, remain to be seen, yet the blockchain ecosystem continues to thrive. Polygon Network (MATIC) is a great example of the talent and capability that exists in India, as is WazirX. We believe that though regulations and regulators are less than friendly at the moment, the sheer weight of talent present in the ecosystem will begin to have a far greater impact on the direction of the ecosystem, both locally and globally, in the not too distant future. If key stakeholders do not see this direction as positive, they will simply leave and relocate to friendlier jurisdictions. We have already seen this in the world of Web2, and Indian technologists are nothing if not mobile; a delicate balance must be struck.

Read more about Indian crypto regulations here.

Looking Ahead - A SWOT Analysis

We’ve presented you with what’s been going on around the world and how regulatory frameworks have been evolving and developing in several jurisdictions. Though this information is both important and (hopefully) useful, understanding how it fits into the broader context of the macroeconomic environment is challenging. As such, in this section, we will present our perspective on how we think the development of the space will progress in the coming years to give you some extra colour.

It is important to remember that what is said hereafter is purely opinion and should be treated as such.

Strengths

Despite the ongoing market meltdown and the implosion of several notable protocols and projects in recent months, the space has demonstrated unprecedented resiliency. We wrote about the collapse of Luna here, and one of the key takeaways from that piece was that no third parties had to step in to create stability. There has been no radioactive fallout, and the broader macro environment remains untainted by what has been going on inside of the experimental crypto reactor. Since that point, other significant players in the space have also been stress tested to the nth degree. This is a good thing, the pain separates the wheat from the proverbial chaff. To quote Warren Buffet, “when the tide goes out, you can see who’s been swimming naked”, and with high profile, black-swan-esque collapses of protocols that many would have assumed were too big to fail, it seems that swimwear is in far shorter supply than anticipated.

Those who are adequately dressed are just about surviving; some have even been thriving. Many, however, have been found aimlessly floating, and even with the majority of assets down well over 90% from ATH, no third-party traditional finance players have had to provide aid. The likelihood of an external intervention is very low, (barring something truly exceptional) and every day we survive lends further credence to the remarkable resilience and maturity of the space.

Weaknesses

As stated above and in our recent article that took a foray into Goblin Town, many market participants and projects have fallen >90% from their peak valuations. Many of these projects will also still be massively undercapitalised, and the teams running the show may also lack both bear market and business experience. This is a recipe for mismanagement, misallocation, and potentially misappropriation of funds.

To that end, it is not unreasonable to anticipate that there will be more pain and more high-profile implosions, possibly from participants at the level of Celsius and 3AC. These household names going under demonstrate if your business model is flawed and your risk management strategy is faulty and your core starts to overheat, it doesn’t matter what your TVL is, how good your research is, or how much clout you have on Twitter. Your days are numbered, there are red candles in your future, and catastrophic failure is all but inevitable.

Opportunities

This period of market activity combined with ever-increasing regulatory clarity presents many interesting areas of potential opportunity going forward. Those who survive this downturn will be proven bear market survivors with a (hopefully) viable business model in an increasingly unambiguous regulatory environment. Though the space dynamics will probably change from what we know now, with retail investors potentially being further limited in the protocols and primitives that they can engage with, compliant rails for institutional money may well exist. If that is the case, then “the institutions are buying” will no longer be a meme, and the wider adoption that many anticipated coming to this cycle will be brought about. Projects built with compliance in mind are likely to boom in this period as they already have the safety measures and mechanisms in place that the regulators will be looking for when they come knocking.

It is then also likely to become clear which jurisdictions have got it right with regulation and where the value of the innovation blockchain is delivering is being captured. Decentralised teams are nothing if not mobile, so it is not unreasonable to expect movement.

Further to the above, crypto M&A season is beginning in a similar manner to the acquisitions following the implosion of Lehman and the 2008 financial crisis. Cash-rich projects during a market downturn have the opportunity to acquire assets, external projects and poach teams which ultimately add value to their business ecosystems. We are seeing this with Nexo offering to buy the Celsius loan book and FTX bailing out various projects in distress - most notably this week by offering $250M and $200M lines of credit to BlockFi and Voyager respectively. Ultimately we speculate that FTX will end up owning a large swathe of the entire digital asset space carrying parallels to how Nathan Rothschild virtually bought the Bank of England in 1815 following the Battle of Waterloo.

Cash-rich, intelligently and sustainably run businesses through the bull phase of this market will ultimately position themselves as victors through the bear phase by striking whilst the over-leveraged and poorly run institutions begin to flounder. Looking at the type of M&A activity which happens in traditional markets in a downturn, we can expect further consolidation and acquisitions.

Threats

There is no opportunity without risk, and risk is ever present in a market as volatile as crypto. We see the majority of risk coming from the global macro environment, which means it doesn’t matter how safe or well built our experimental crypto reactor is, because an earthquake could render it all useless. The world is facing the strongest economic headwinds of a generation. The fallout from COVID, the impact of laissez faire money printing, supply chain shocks, war, and global food supply issues are coalescing into a maelstrom of pain and uncertainty. If we had a crystal ball, we could share some insights when this will end, but we do not, and when this will stop is anyone’s guess. As such we can only advocate a highly risk averse approach for the foreseeable future. In future articles we will outline our current macro investment thesis and strategies in-depth.

Friendly regulation is also not a guarantee of a positive outcome, as implementation is down to the regulators. Regulators are people and will have their own opinions, biases, political leanings, and perspectives on how the space develops going forward. This is why it is so important to keep the regulators onside and to work with them wherever possible. As we touched upon earlier in the context of marketing, everything starts with education. If the space understands this, and open dialogue is maintained in the spirit of mutual benefit, we can all achieve great things. If the opposite is true, and the us vs them mentality continues, it will be a bumpy landing.

Conclusion

Regulation is needed more than ever due to current events within the lending ecosystem (Celsius/3AC) and the stablecoin ecosystem (LUNA/UST). However, for regulation to be successful, it must be accommodative to growth and evolution whilst protecting market participants and the wider financial system from any insidious systemic risk. Managing the delicate balance between delivering economic benefit, protecting the average consumer, maintaining political stability, and protecting national interests is the name of the game. Multiple jurisdictions are taking a variety of approaches when walking this tightrope, and with the passage of time, the right approach will become evident.

Without a solid regulatory framework, there will be no real utility for crypto and blockchain technology. Regulations are the needle that will burst the bubble and reset the playing field, allowing a new cycle to commence based on real-world applications, not the speculative frenzy we have witnessed since the 2020 COVID crash.

You should be excited about regulation, as it will finally propel crypto into the mainstream and remove the red tape prohibiting the bigger, slower-moving institutions from getting involved. With this barrier removed, and the enormous amounts of idle capital that could be unleashed, building unlike anything we have seen before will likely commence.

Specialist Insight

Accessing top-tier professionals and content in the crypto space is not generally something the average retail investor can do. That is why we will be looking to leverage our shared industry networks to deliver some extra value to readers - asking important questions to deliver real insight from those working at the forefront of the space. We are committed to making institutional grade asymmetry as accessible as possible. We hope that what is provided in the specialist insights section will be useful to you on your digital asset journey.

Our first specialist in this regard is Oskar Åslund. Oskar is the Head of Business Development and Token Operations at AK Jensen. AK Jensen Group Limited and its subsidiaries, established in 1995, are owned by shareholders who collectively have over US$24 billion in assets under management. The group serves hedge fund and institutional clients in 35 countries worldwide. AKJ has won the HFM Best Hedge Fund Platform award six times over the past seven years.

Oskar joined AK Jensen Group in 2017 to lead the AKJ Crypto Hedge Fund Platform and the AKJ Token development. In his role at AKJ, Oskar works together with the hedge funds on the platform to enable competitive and compliant crypto trading solutions. Oskar also sits on the board of 20+ crypto funds, most of them regulated by FCA as IAFs. Before joining AKJ, Oskar co-founded Blockchangers AS, a leading blockchain consultancy firm in the Nordics, alongside being a public speaker on blockchain technology. He is part of the team behind Oslo Blockchain Day, the main blockchain conference in Norway.

Q. What are the current market trends regarding new interest and has the downturn affected that interest?

A. Yes, for the moment, most investors are waiting out the turmoil and the new inflow has halted due to the extreme circumstances. It's a bit unfortunate (for the investor), but it's easier to get new money into Crypto when prices are higher in the bull markets.

Q. What are the demographics of new investors? Is interest more from institutions, HNW individuals, pension funds, and sovereign wealth funds?

A. We see most interest from HNWs. Many institutions are opting not to buy this dip currently - we mainly feel that this is due to the wider macro headwinds, risk-off stance in global markets and fears of inflation etc. On a positive note, we have seen people with dry powder and experienced crypto prop traders continue to increase their holdings and DCA at these depressed prices.

Q. What are the biggest risks AKJ can see in the future development of the space? Are they internal or external risks?

A. I'd say that regulators/governments try to favour CBDC’s and believe that these should replace rather than coexist with open-source crypto networks is a large external risk. As for 'internal risks', these will organically come and go, and there will always be counter-movements and lessons learned. The LUNA/UST collapse is a good example, it hurts for some and may have spillover effects, but it's within the expected 'creative destruction' that comes with innovation.

Q. Has there been a shift in the attitude of the regulators at all in light of recent market and geopolitical events?

A. I think now they are more confident that they can step in and establish regulations that can be pretty upsetting at first. But in the long run, that will be for the better, with more certainty and less investor risks, and it will bring full acceptance for the asset class. But some values will change along the way, and those who want an alternative financial market that is 'KYC free' and where services are fully permissionless, may not get it their way. I don't see that DEXes with anonymous LPs and permissionless listing of tokens is the future after all regulation is in place and enforced globally.

Q. Is there a particular subsect of the web3/crypto space that is receiving more interest than others, and if so, why do you think that is the case?

A. Obviously, Metaverse, NFTs and Gaming have been huge lately. We are starting to see the first funds that are not just 'Crypto' but actually focused on these industry segments. The interest is partly for a good reason, these sectors will see a lot of value creation over time, but there has obviously been much more hype and short-lived bubble economics than sustainable adoption. I don't really think that NFTs or Metaverses that are popular now and had high valuations before this crash will see sustained interest and real adoption. Especially Metaverses may be very hard to tell whether they will get any adoption or not. Just like with social media, only a tiny % of all attempts become the Twitter, Facebook and TikToks of this world.