Ponzi Schemes, Carrots and Sticks - The Use Of Incentives In Blockchain

Ponzi Schemes, Carrots and Sticks - The Use Of Incentives In Blockchain

When, Why and How are Incentives Used?

Disclaimer: Any views expressed in the below text are the personal views of the author/s and do not constitute investment advice or recommendations for investments. The author/s views should not form the basis for making investment decisions - invest in markets at your own risk after performing thorough due diligence.

Let’s take a walk down memory lane. You’ve just finished eating dinner, but your parents asked you to help tidy up. You immediately and enthusiastically made clear that this is not something you want to do. One of two things then likely occurred. Either they said that if you helped, you could have something you wanted or alternatively they lovingly informed you that if you didn’t help, you would lose something you did not want to. You were offered a carrot (an incentive), or a stick (a disincentive). Maybe a dessert was on the line, watching an episode of your favourite TV show, or perhaps something else entirely.

An incentive encourages certain behaviours in return, whereas a disincentive uses something to discourage or deter certain behaviours. These concepts are used in the workplace in the form of financial bonuses for hitting a target or in parenting with the loss of certain privileges.

Though perhaps not as obvious as the above examples, incentives are everywhere in the blockchain. Layer-1s use block rewards and transaction fees, Layer-2s love an airdrop, DeFi protocols and DAOs offer high yields.

This article will examine the rationale behind incentives and disincentives, the applied concepts, alongside highlighting some projects that we feel are establishing themselves around these core principles. Let’s dig in.

No Man Is An Island

In the immortal words of John Donne, “no man is an island.” This means that, for better or worse, we frequently need to collaborate with others. This could be a part of a department at work, a study group at school, or a sports team. Sometimes it’s a match made in heaven, and collaboration with another comes as naturally as Peter Schiff predicting the decline and implosion of Bitcoin for the nth time before breakfast. Other times it can be a less enjoyable experience, more akin to buying the top of $LUNA and once again acting as someone’s exit liquidity. Our interactions with others in both instances need to follow rules to ensure effective collaboration. These rules will still need to be followed even if it feels like everyone else is acting out of self-interest.

The tragedy of the commons is an excellent example of the impact self-interest can have, and though you may not realise it, you’ve likely experienced it. It’s a situation where individuals with access to a public resource, known as a common, act in their interests and everyone else second. In doing so, these individuals then deplete the resource and exploit it for their interests alone and fail to consider the greater good or long-term sustainability of such resource use.

So, what can we do about it?

Incentives and disincentives make it possible to counterbalance the individual's self-interest. It is possible to align that self-interest with the broader group instead.

Figure 1 - Traffic congestion is another example of the tragedy of the commons. Taking a car is generally faster than public transport, but when everyone does it, the opposite becomes true. Source: ABC News

Incentives in Blockchain

The issues commonly seen in blockchain, which tend to be Ponzi schemes, implosions or other irregularities, are also seen in computer science and different types of networks. To solve this problem and for a network or system to function as intended, those parties must behave in a way beneficial to that network or system.

Blockchain is rife with opportunities to put self-interest first. There’s nothing wrong with acting this way, as no one will look after your interests but you. Even taking profits is an example of this, though not an easy one for most people.

To mitigate this, we create a set of rules or a framework that reduces the risk of self-interest being the most attractive motivator. These rules should also encourage the needs of the blockchain network or protocol to preferentially be met.

Therefore, the incentives/disincentives should be designed so that an individual is better off playing by the rules than breaking them.

Figure 2 - Scams like the above result from a misalignment between the interests of the scammer and the wider community. Source: Moralis Academy

Network Level Incentives

Base-level blockchain networks typically use transaction fees, block production rewards, or both as a part of their incentive and reward structure.

Transaction fees, though sometimes expensive, are essential as they serve a dual purpose. First, they incentivise a block producer to include a given transaction in a particular block. When a network is clogged and many transactions need to be confirmed, paying a higher fee is one way to ensure your transactions go through. Users who pay a higher transaction fee are more likely to have their transactions confirmed first. It is ultimately more attractive for a block producer to include that transaction than not - their self-interest aligns with the user's interest.

Second, transaction fees mean attacks cost money. Attackers have to pay a transaction fee for each submitted transaction. Unless the attacker stood to gain something significant, the attack would quickly become economically unviable. Therefore, it would likely no longer be in the rational self-interest of the attacker to conduct the attack.

Next up, there are block production rewards. These tend to be issued to network participants that support the network in producing new blocks, such as miners for Proof-of-Work (PoW) or validators for Proof-of-Stake (PoS). The block producers leverage a resource of some sort, computational power for PoW or stake for PoS, in support of the network, and are rightly compensated for doing so.

Block rewards are, however, not constant and reduce over time. In Bitcoin, block rewards half every 210,000 blocks, so miners lose revenue. This is where transaction fees come back into the mix, as they are what is supposed to keep the Bitcoin network attractive and lucrative for miners. Whether this will actually be the case long-term remains to be seen.

Figure 3 - Bitcoin block rewards drop over time. Every block mined yielded 50BTC before the first halving. By 2032, each block will yield less than 0.7BTC. Source: BTCsv via ZDNet

Disincentives are more common in PoS networks. If a user becomes a validator in a PoS network, they commonly have to lock up a portion of their stake to run a node. In running a node, they can choose which transactions are included in a given block, which begs the question, “what’s to stop a validator from including the wrong transactions?”

This is where slashing comes into play, where a user is punished for including the wrong transactions. If a validator is found to be including “incorrect” transactions in their blocks, then depending on how the protocol is designed, they can lose their stake in the network. This also applies to other users who have delegated their stake to a validator, which is why choosing honest and reliable nodes are essential. Punishment can also be levied if a validator is offline for too long, so there are potentially two sticks at work in a given PoS network.

To summarise, the primary rationale for block rewards and transaction fees is to reward users for productivity and disincentivise harmful actions.

Protocol Level Incentives

So far, what we’ve covered has been solely focused on Layer-1, the base layer blockchain, but what about DApps and DeFi protocols built on these chains?

How does a dev team get people to use their platform?

Incentives.

New protocols and platforms need liquidity more than anything else at their deployment.

Depending on the nature of the protocol or specific team, liquidity may be difficult to obtain. This difficulty can be offset through incentives and is where you’ve probably heard the term yield farming. Yield farmers are investors or users that provide liquidity as Liquidity Providers (LPs) in return for a fee.

Specific protocols attract yield farmers by running liquidity mining campaigns. These campaigns offer increased yield for a set period, which can boost overall platform liquidity and attract more users to the protocol. These short-term incentives are attractive as they provide a higher rate of return than conventional savings rates and are often around 4-8% APY.

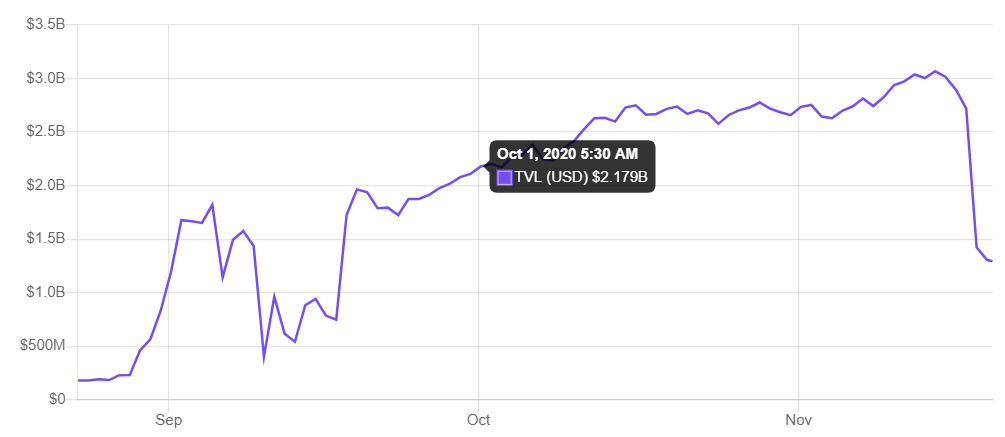

Incentives are sometimes even higher, however when the incentives run out and the campaign finishes, there’s very little reason for the opportunistic yield farmers to remain. If there’s better ROI elsewhere, farmers will leave. This is what happened with Uniswap in November 2020, where TVL dropped >50% at the end of a liquidity mining campaign.

Figure 4 - Uniswap TVL drop in November 2020 at the end of a liquidity mining campaign. This liquidity moved to other Dexes still offering rewards. Source: DeFi Pulse

In this instance, mechanisms need to be implemented to ensure the end of a campaign doesn’t result in a drop in liquidity. This can be achieved with a token lock, whereby there’s a remarkable down period to remove liquidity, or through bonding, whereby the protocol purchases the LP tokens.

Bonding potentially allows investors to receive tokens at a discount to the market rate and reduces the risk of a sudden liquidity loss to a protocol.

Potential yield with these mechanisms can sometimes be insane, offering thousands of % APY. A higher APY could be seen as more attractive to a possible LP, so protocol teams may use these in the short, or even the long term.

If a long-term strategy is taken, then something else is needed as well: a narrative. This is precisely what Olympus DAO, and the cutlery drawer of forks, sought to do with (3, 3). The basic premise of (3, 3) is that a user stands to make a greater return on their investment if they cooperate with other users. The irony here is that cooperating with other users and not selling is actually a worse choice for the individual, and reaches something called Nash Equilibrium.

Figure 5 - (3, 3) is bad for both suspects as they both receive the blame, but if they’re both to blame then no one is to blame. Think of it like an inverse win-win - if you’re both wrong, you’re also both right. Source: Corporate Finance Institute

With Olympus and OHM, if everyone keeps their tokens staked, supply is reduced and demand increases due to reflexivity alongside token prices. This is a great idea on paper. However, it makes one fatal assumption. The prisoner's dilemma only works to everyone's benefit if all parties involved are rational. If you’ve spent any time on crypto Twitter or in telegram groups, you already know this is far from the case in the land of crypto.

Oympus DAO used a game theory thought experiment as a core reason for existence - the prisoner’s dilemma.

What ends up happening is that while some will be sucked into the narrative of the (3, 3) greater good story, more ruthless and seasoned investors simply dump their tokens. Their self-interest is in seeing a return, not in making everyone else richer.

Steps have been taken to address this, however, namely through inverse bonds. The Olympus protocol will repurchase tokens at a premium to the current market rate, which is an innovative way of trying to bring self-interest and protocol interest back into alignment. As with all things blockchain, it’s a novel concept, so the long-term efficacy is anyone's guess.

Figure 6 - Olympus DAO, pioneer of Ponzinomics and everyone’s favourite scheme. Source: LinkedIn

Airdrops

This brings us to the last significant incentive we’ll cover in this piece: airdrops.

The best way to think of an airdrop is like a mystery box for performing a task. Many Layer-2 or DeFi protocols use airdrops to bootstrap their user base through bribery. The premise from a user perspective is that by interacting with a new blockchain or DeFi protocol, may yield a reward in the form of an airdrop at some point in the future.

The potential promise of a reward may not sound enticing. Airdrops are often just rumoured, not announced, and the actions one needs to perform are not usually known. There’s also a cost associated with using a new protocol, so why do so many users try to game the system and farm airdrops?

Self-interest.

Some airdrops have been massive in their total value, so the potential for a stack of free cash is a giant carrot. Taking Uniswap again as an example, early users of the protocol received an airdrop of 400 UNI tokens. These were worth $3,300 at the time of the drop. This meant the total airdrop value came to >$1 billion.

Airdrops are also great from a developer standpoint. They encourage users to engage with the platform, provide data, generate revenue, and build a community around whatever they’re building. Sharing a bit of that new revenue is a small price for making a name in a new industry, as what can be gained is far more valuable. It’s in the self-interest of the dev team to share that newfound wealth.

That being said, airdrops are also a potent marketing tool. In many instances, token value plummets after a drop has been made, as users have got what they came for, so why stick around? For more info on this trend, check out this article from The Defiant.

Figure 7: 1inch TVL before and after the airdrop. No prizes for guessing when it happened. Source: DeFi Pulse

What Happens When It All Goes Wrong?

Incentives and disincentives, though useful, should be used carefully. If the incentives a protocol gives out are not sustainable from a business model standpoint, you have a problem. The best example of this has been seared into the memory of everyone in the blockchain and crypto space: Luna. We’ve written about the Do Kwon/Terra Luna fiasco extensively here. The short version is the yields on offer through Anchor protocol did not align with the long-term stability of the protocol. The only way to keep the money was to bring in new users.

There’s a name for this: a Ponzi scheme, so it probably is when something seems too good to be true. This is why appraising the business model, and tokenomics of a protocol or network should be at the core of any strategy. Sustainability is what will separate the wheat from the chaff.

Figure 8 - The Luna collapse. This looks healthy. Source: TradingView

Equally, if incentives and rewards are offered, those with the means to claim a larger share of those incentives will do so. This is a big issue with PoS networks, as rewards are distributed deterministically. This means they tend to go to the validators with the largest stakes. Similar problems can also be seen in PoW networks with the emergence of huge mining pools. The likelihood of mining a block increases relative to computational power, so there’s an incentive to pool power to increase the chance of sharing in the rewards. Another issue to be mindful of is the potential for pseudo-centralisation to occur with time.

This will begin to look like centralisation over time, so mechanisms must be implemented to incentivise the opposite. Networks like Cardano, for instance, reduce the rewards a validation pool receives once it grows beyond a specific size. This way, users are incentivised to delegate to smaller nodes, which encourages decentralisation. This approach rests on the assumption that decentralisation is desirable to maintain, which may or may not depend on how blockchain technology is applied in the future. Still, being mindful of this when doing your research is a consideration.

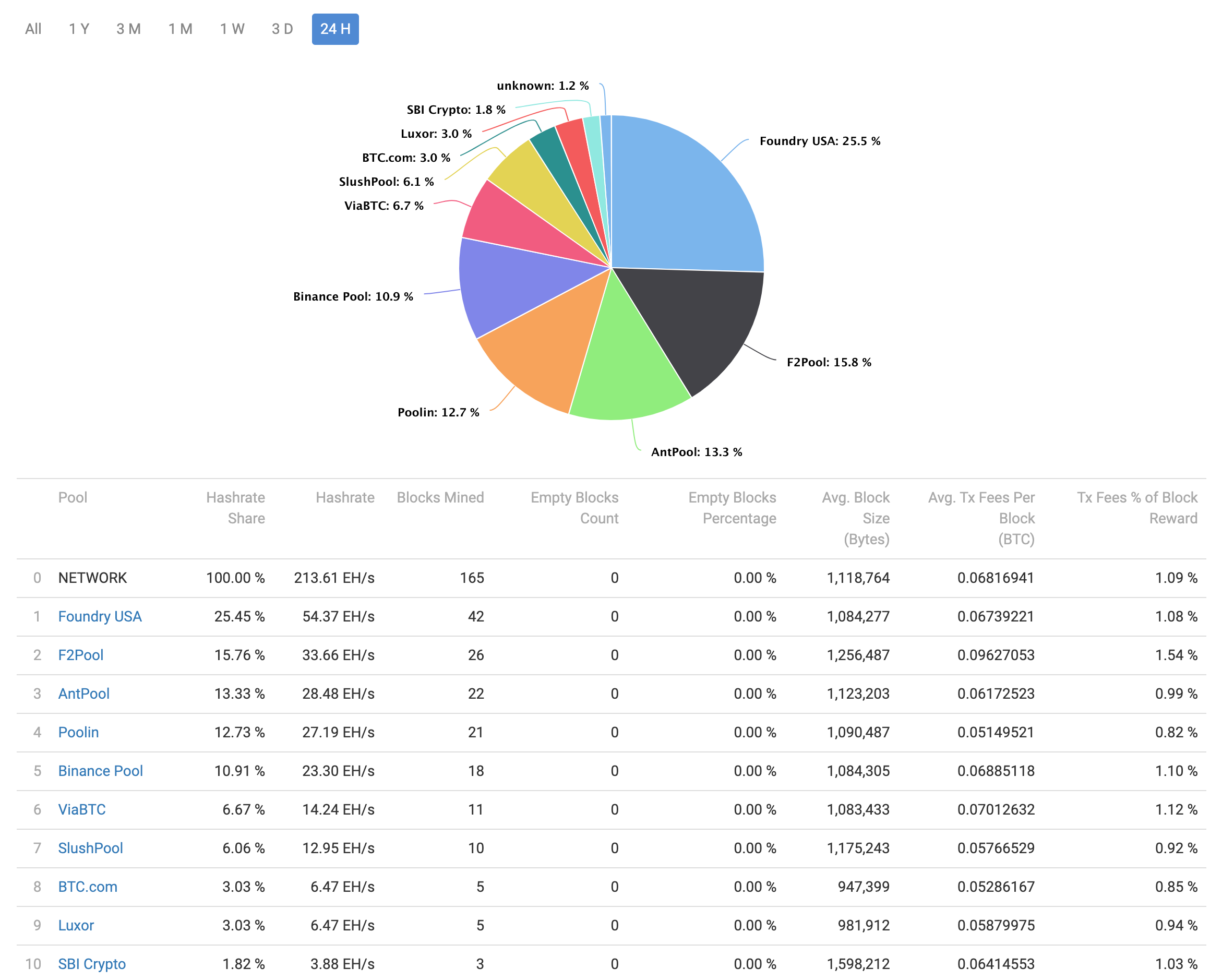

Figure 9 - The top 10 mining pools on the BTC network as of 24/08/2022. The top two mining pools alone control >40% of the network and the top three >50%. If these pools were to collude, then a 51% attack would be possible. Incentives can be used to reduce the prevalence of such large pools and discourage their emergence. Source: BTC.com

Notable Projects

In this section, we’ve selected some projects that are making exciting use of incentives in their design. This is in no way an endorsement of these projects, and further research is advised on the reader's part. Incentive schemes in blockchain are ever-evolving, so what works today might implode tomorrow.

Olympus DAO is the grand-daddy of the game-theory storytelling narrative, so it’s impossible to ignore the impact Olympus has had on incentive use crypto. They’re also doing some exciting work around building novel incentive structures such as the inverse bonds we mentioned earlier. They are working on several new ideas in the future. The protocol also holds, as of the 24th of August 2022, >$287,000,000 in the treasury spread across 50+ tokens. The protocol also owns >98% of the available liquidity, so it may be sustainable in the longer term. That said, it might also just be a Ponzi with enough holdings to not implode yet, so DYOR.

Figure 10 - Olympus DAO pioneered the (3, 3) narrative, spawning more forks than can be counted. Most of the forks are dead, but Olympus is still going. Source: Olympus

Gitcoin is a DAO that incentivizes developers to work on open-source projects. The project’s founders recognized that many software startups end up abandoned, suffering from a lack of financing and (above all) developmental work post-release. Open-source technology solves these issues by allowing customers to freely use and modify pre-existing software and even distribute homemade variations.

Gitcoin leverages hackathons, bounties, developer grants and quadratic funding to keep developers engaged and open-source projects growing Gitcoin has provided over $50 million in funding for open-source projects that may have otherwise disappeared. Incentive use in this way is a powerful motivator for individuals looking to support the projects they love and gain some recognition for it.

Figure 11 - Gitcoin is a DAO that provides incentives for open-source projects and development. Source: Gitcoin

Summary

Incentives and disincentives make it possible to counterbalance the individual's self-interest and align it with the broader group instead.

Careful and considered use of the right incentives can help with protocol growth by aligning the users' interests with a given network or protocol’s needs.

Negative behaviours can be discouraged and positive ones fostered at a Layer-1, Layer-2, protocol or network level.

Yield is a powerful motivator for sourcing liquidity, but when yield drops the opposite can be true.

Incentive structures can encourage either centralisation or decentralisation over time. This isn’t always a bad thing, but must be taken into account.

Incentive structures must be well-designed and sustainable; if they’re not then the protocol is either a Ponzi scheme or it will implode.

Many game theory-based incentive structures, such as (3, 3), are flawed in their assumptions about rationality but are a step in the right direction.

Sustainable business models will separate the winners from the losers in the long run, so if something seems too good to be true, it probably is.